So, when you look at the website of a digital-only bank, there is usually a very clear value proposition, with little obfuscation and jargon, one main message and no complex muddle of products.

I’ve rounded up five financial services websites with crystal clear value propositions, to see what incumbents can learn.

1. N26

In case the homepage pictured below leaves you in any doubt, N26 is a mobile bank. The tagline, “Run your entire financial life from your phone”, is about as clear as it gets, and N26 makes sure that the calls-to-action on the page (‘open bank account’) emphasise the ease with which consumers can sign up.

The straightforward language is continued on the bank account product page. “You’ll never have to visit a bank again” – this takes what for some consumers is a negative of online banks (lack of branches) and spins it as a positive for the more mobile-savvy consumer who never wants to stand in a queue.

N26’s homepage is matter of fact in stating the benefits of its accounts. There’s little fluffy copy – “Open an account in under 8 minutes, withdraw from any ATM….get realtime push notifications with every transaction.”

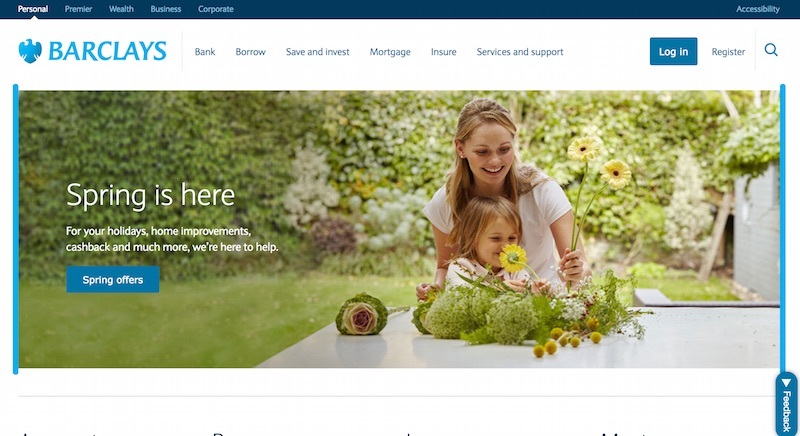

Note that for all of the companies included on this list, images of the mobile interface are a vital part of marketing to their potential consumers. The interface is the product, just as much as the pricing details. Note, too, the lack of lifestyle images of smiling families that one typically sees on incumbent bank websites (here’s an image of the Barclays homepage above the fold at time of writing). Objects are captured to show the bank’s place within a busy lifestyle (sun hat, passport, keys), but it is the product that inspires trust, not a persona.

{kind=link}

The ‘8-minute’ proposition is rammed home again when the user clicks to open an account, a nice touch to chivvy the user along.

2. Trov

Trov offers on-demand insurance. Here’s an instance where images of people are appropriate, with the guitar-playing beach bum a strong indication that this insurance product is not as stuffy as all the others, and befits a roaming lifestyle.

Illustrations are used effectively. The message format is second nature to younger demographics and its inclusion here is a powerful indicator of a product that works on their terms.

Clicking the ‘How it works’ button in the top menu gives a very simple light box which demonstrates key features of the app. Once again, this is a very obvious example of a company selling the experience over and above its pricing.

3. Acorns

Acorns is a micro-investment platform. The website is particularly good at communicating what the app does. That starts with some confident copywriting – ‘Automatically invest life’s spare change’, followed by the assertion that ‘anyone can grow wealth’.

Acorns is very good at explaining how the app works, breaking the process down into three steps. The screenshot below shows the advantage that such focused apps enjoy over competition that provides multiple bespoke services – Acorns is able to distill down its proposition. Clarity is one step away from transparency, giving the consumer confidence.

Security is one marketing message that new fintech players have to convey, where incumbents can perhaps rely on their reputation as safe places for your money. Acorns’ website addresses this issue, stating its ‘serious security’ credentials, including its membership of the SIPC.

The $1/month pricing is attractive, offering little barrier to virgin investors, and the Acorns website lists exactly what such a modest fee gets you.

Lastly, I was impressed by the educational content on the Acorns website, designed to make sure its target customers do not feel out of their depth. There’s a particularly good explainer video (clickable, too) and an FAQ-style section with some very simple questions answered, such as ‘what is an ETF?’

4. ClearScore

ClearScore is one fintech company that is synonymous with clarity and great UX. Its homepage is probably the best and clearest value proposition in the sector.

ClearScore uses the language of enfranchisement – ‘your credit score should be free’. And powerfully declares ‘Just free. Forever’. This proposition had a big effect on the competition, which followed suit in offering a free score.

Compare ClearScore to incumbent Experian, which looks pretty similar but notably includes much more information to try to assert its trustworthiness and functionality. ClearScore lives up to its name with a website that appears to exist simply to show the consumer their credit score, which is exactly what they want.

ClearScore even dares to declare its credit report beautiful. Again, the company is appealing to the part of the consumer that is fed up with wading through financial guff.

The brand tries to be as transparent as possible when it comes to data, spam and risk-free score checking. These values are important to consumers who don’t want their score or their inbox to be compromised simply because they are seeking information in order to improve their situation.

Testimonials offer further assurance.

5. Stash

Stash is another investment platform, like Acorns, which promotes small investments and low fees.

Stash uses similar messaging to Acorns but has a bit more emphasis on empowerment, rather than the ease/low risk which Acorns promotes. Stash appeals to a ‘new generation’ of investors and talks about its ‘mission’ to give everyone access to financial opportunities.

Furthermore, Stash promotes investment portfolios that mean something to the investor.

The ‘invest in what matters’ line is backed up with visuals that represent a range of ETFs, each with their own snappy title (see ‘delicious dividends’ further below).

An investment calculator with a slider helps small investors to project the success of their funds over the next 20 years – a powerful motivator to start today.

In summary…

There are some obvious tropes used by these websites, each of which boils down to a focus on UX and transparency. Bold copywriting without too much detail, beautiful shots of the app interface, and calls-to-action to start today are all common place.

It’s not hard to see how, according to a new study conducted by PricewaterhouseCoopers, established financial services firms could lose 24% of their revenue to fintechs in the next three to five years. As my colleague Patricio Robles points out, fintech startups ‘largely don’t have to worry about large legacy systems, and their priorities aren’t pulled in a million different directions because they don’t have a million different lines of business.’ This is evident on their websites.

Incumbents are fighting back though, with mobile functionality and online services given more elbow room on the homepages of big banks, for instance. As reported by The Financial Brand, the incumbents are still in a very good position considering the ‘stickiness’ of customers in financial services, particularly banking.

Challenger banks in the UK face an uninspiring average annual population growth rate (less than 1% over the last five years), and despite efforts to simplify the switching process, the Current Account Switch Service program has seen only 3 million accounts change hands since inception, roughly just 1.1% per year.

One thing is for sure, though, those that do switch to new banks, insurers and the like can be fiercely loyal to those companies they see as tech and customer service pioneers. The 2017 Monzo outage proved that even in the face of failure, honesty and simplicity are strong brand characteristics.

Comments